The Fed’s Last Stand: A Solitary Rate Cut Expected for 2024

As Spring begins to fade, the continuation of uncertainty on interest rate cuts remains of paramount importance.

We continue to believe that at least one rate cut is possible but likely later in the year. However, with the economy proving to be fairly resilient and inflation relatively sticky at these levels, the decision will likely be tied to the strength of the consumer. What we have noticed there is that while consumers have kept their wallets open, their spending patterns have begun to adjust as a result of persistently high inflation and increased borrowing costs. Most of the changes have been visible among middle- to lower-income households—many of whom had depleted their savings buffers built up during the pandemic—whereas higher income households still appear to be spending at full tilt.

Investors should therefore be careful and adjust their portfolios accordingly, including adding more defensive positions. The market does not appear to be overvalued at this stage given the recent earnings, but there are certainly names with high multiples that need to be repriced if rate cuts are pushed further out. We have already seen this adjustment begin over the past couple of months.

Bonds corrected swiftly to the news—equities, meanwhile, did not fully price in the deferral of rate cuts, leaving more room for volatility on that side of the portfolio.

Overall, investors seem reconciled to a single rate cut for the year. We have, however, noticed a disconnect between the bond and equity market responses to the postponements. Bonds corrected swiftly to the news—equities, meanwhile, did not fully price in the deferral of rate cuts, leaving more room for volatility on that side of the portfolio. If inflation remains sticky throughout the coming months, as it has in the first half of the year, the U.S. Federal Reserve (the Fed) could once again delay the timeline and cause the latter to catch up.

The Stronger-for-Longer U.S. Cycle Marches On

U.S. economic data remains remarkably buoyant, with Q2 growth flirting with an astonishing 4% annualized rate. In Canada, central bankers are far, far closer to commencing much-needed policy relief.

U.S. Outlook

Canada Outlook

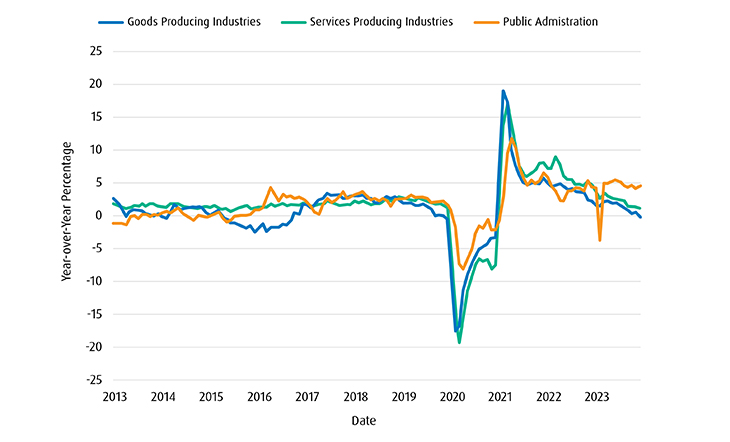

The good news is, we are not talking about a recession—but we are flirting with one, to be sure; the gross domestic product (GDP) print for February came in below 1% (year-over-year), whereas the U.S. is north of 3%, and cruising at that altitude. That speaks to two completely different economies. The rate shock is the key driver behind that growth differential and the bad news is, it is going to get worse before it gets better. The bulk of residential mortgage refinancing is ahead. Labour shortages continue to mitigate some downside risk—which could prevent a recession that would normally come with a rate hiking cycle. Interestingly, when you look at public sector employment versus private, the former is running at a 4% growth rate (year-over-year), and the private sector is basically flat.

Public vs Private Job Gains

Source: Statistics Canada/Haver Analytics.

So, who is feeling the rate impact? It is private sector workers, who are not getting pay increases compared to government staffs. That dynamic is strengthening the conviction at the Bank of Canada to start cutting benchmark rates. There is mounting data to justify rate loosening as soon as June. Maybe they wait until July, but the data is very loud and the growth outlook very weak. It is time to cut.

International Outlook

In Europe, economic data are coming in better than expected, which is important because global growth is now not only being driven by the U.S.; we’ve seen the bottoming out for Europe and now momentum is improving—it is not booming, but nevertheless strengthening, which should continue as we move further into the year and the European Central Bank (ECB) moves to cut interest rates. It is practically a done deal, the ECB having indicated that it would take something very unusual in order to not cut in June. The big question is how much monetary easing to deliver in the next 12 months. That will be data dependent, but we would argue that the overall data and inflation in particular will warrant about 100 basis points of cuts.

Key Risks | BMO GAM house view |

|---|---|

Recession |

|

Inflation |

|

Interest rates |

|

Consumer |

|

Housing |

|

Geopolitics |

|

Energy |

|

Asset Classes

It is premature to point to some recent economic and earnings disappointments as evidence of a trend taking hold. Inflation adjusted growth remains strong in the U.S., with bond markets adjusting accordingly.

Is there reason for caution? Yes, but how justified it is depends on your focus. In arriving at our Five Lenses outlook, we evaluate available data and information across four pillars: the economy; fundamentals; policy and behavioral, or market sentiment. Policy and sentiment have been the driving forces over the past month or so, at the expense of fundamentals and the economy. The market overreacted to one disappointing GDP print that came in low versus expectations. But below the headline, it was a function of exports falling down—more simply, the rest of the world not buying enough stuff from the U.S. That event coincided with some slightly bearish earnings reports, led by Meta Platforms, Inc. Investors who had been looking for a reason to get upset found a few that day, and the market reacted predictably. However, when looking at nominal U.S. growth, it remains strong, although variation in the final leg of the Fed’s inflation fight will invariably lead to some dips on an inflation adjusted basis. We won’t rush to judgement on whether we are seeing the beginning of a negative economic trend quite yet.

We’ve seen plenty of upside surprises through earnings season. Unfortunately, they have also been paired with some very big disappointments from some mega caps—healthcare in particular, with Bristol Myers Squibb posting a sizable drop, due purely to a one-time charge booked related to an acquisition. Volatility is rising, with not much upside price reaction even on strong earnings or revenue beats. However, on an absolute basis, it is hard to argue that this earnings season has been anything other than strong, despite some key mega-caps disappointing more enthusiastic investors with more tempered sales expectations for the quarters ahead.

On bonds, Fed commentary has become more hawkish, but the market—as it always does—has jumped ahead and said, “Well, if you’re not going to cut, that means you’re going to hike.” This seems a fairly broad leap of logic, as the market is still pricing in at least one, maybe two cuts by year-end The U.S. economy has adapted so far since last December’s overly optimistic view of 6–7 cuts, but as soon as the real prospects of hiking become reality, that may change. A 10-year U.S. bond back above a 5% yield is seen as an important psychological level, which should coincide with significant institutional demand. Nonetheless, we’re still neutral on Duration1—we’re not brave enough yet to really go short at this point, given the high volatility in the rates market.

EQUITIES

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

FIXED INCOME

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

CASH

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Equity

Earnings season revealed a broadening of the Artificial Intelligence (AI) cycle into other sectors. U.S. market leadership remains firmly intact but high valuations and strengthening momentum elsewhere suggest some rotation may be warranted.

First quarter earnings were relatively strong, with average growth of about 5%—and 15% for Technology (Tech). However, this past quarter, despite having the best absolute earning, Tech was not the best-performing sector. That is because the market is reacting to company guidance now beyond just earnings, with Meta being the best example. Their earnings were good, but weaker guidance caused a negative price reaction. This reporting period showed that, given such high expectations for these firms, they need to deliver on earnings and guidance to justify their lofty valuations. From a positioning standpoint, we are overall still neutral on Tech from a sector perspective, and this earnings season just showed why: the bar is very, very high to not only meet but beat expectations. And guidance is an increasingly important factor.

The good news for technology is that a multi-year spending cycle relate to AI is underway. And more broadly, we are starting to see that trend translate into good news for other sectors such as power utilities and data infrastructure—some of the best-performing names in Q1. The market is starting to realize that there are other beneficiaries outside the traditional technology sector coming to the fore.

Overall, U.S. equities is the place to be given the strength in growth, a broadening of positive earnings and continuance of a strong domestic economic backdrop, which bodes well for sectors that are domestically focused, such as industrials. There is the very real re-shoring theme, some AI exposure and electrification and the sector is heavily anchored to the domestic U.S. economy. Our U.S. positions are being funding through maintaining an underweight position to Canada. That said, given valuations, we are looking at a potential rotation away from U.S. exposure, either through closing that underweight to Canada or upgrading Europe. We’re not there yet, but we’re beginning to think about that trade, as economic momentum Europe in particular is rising.

CANADA

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

U.S.A.

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EAFE

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EM

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Fixed Income

Duration yields are edging once again back toward the psychologically important 5% level, though we still prefer a neutral position across bonds until the market has a greater sense of Fed policy direction.

We are in a trade-the-range environment until we see U.S. interest rate cuts. With one or perhaps two priced in for 2024, we are seeing 10-year U.S. bonds moving closer to 5%, or levels that are once again becoming attractive. The bar to cut rates is now high, but in our view, the bar to hike is still higher. If we get to a point where the market completely prices out cuts and 10-year bonds rise above 5% yields, that’s where Duration starts to look interesting again. But right now, we are still within the recent range so we have not moved off our neutral stance. The same can be argued the other way—if we get to a point where the market prices in more cuts, we might start underweighting longer dated bonds, if the markets get too aggressive. Our current view is that pricing is fair, and we are going to maintain a neutral position.

In terms of Canadian fixed income, it is almost the opposite view compared to equities, where we prefer the rest of the world, including Canada, to U.S. bonds. The need for rate cuts is higher outside the U.S. In areas of the portfolios where we have a choice, we prefer Canadian government fixed income to the U.S. given the potential divergence in monetary policy.

On Investment Grade, we also remain neutral. Spreads have come back a little bit, but there is not enough compensation there yet for us to jump in to an overweight position. And we would prefer Canadian or European credit to the U.S. given those spreads aren’t fully valued. It is a similar story on High Yield, with spreads backed up to an extent, but not to the point where it is worth an overweight tilt.

IG CREDIT

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

HIGH YIELD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EM DEBT

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

DURATION

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Style & Factor

Broad market dynamics continue to improve, creating an opportunity for diversification, specifically away from the Mag 7 stocks, which are showing clear signs of momentum fatigue.

We’ve begun thinking about a shift in sector and geographic allocation back towards the Canadian market, while Japan continues to outperform on a relative basis. These developments are reflective of an improving environment for Value relative to Growth. More specifically, what is helping Canada is the pure cyclicality of our sectors (Financials, Energy, Materials), which reflects the emergent Value opportunity. Copper comes to mind as probably the best example of that, while Energy has been doing well too, both in Canada and the U.S.

We are moving away from thinking of “the stock market” as a ubiquitous vehicle, more towards “a market of stocks”, where investors can start differentiating given the divergence among sectors and among individual names. Whether it is Value or another factor, or a sector approach, it is about diversifying away from what has dominated leadership over the past 12 months: i.e., the Magnificent Seven. The group has hit some bumps in the road—and investors are starting to wonder: where will those stocks be by the end of the year? Alphabet Inc. just initiated a dividend, following Meta’s earlier example, and Apple announced a massive share buyback program. We’re starting to see these tech monoliths give cash back, and as Warren Buffett said, you only give cash back to shareholders when you don’t have a better idea about what to do with it. Perhaps Growth won’t be quite what it was going forward, at least for the next little while.

VALUE

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

GROWTH

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

QUALITY

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

YIELD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Implementation

The are multiple concerns that underscore our deteriorating view on the Canadian dollar (CAD). Meanwhile Gold, while experiencing a near-term pause, has room to run amid ongoing central bank demand.

We remain slightly bearish (-1) on the CAD, because of the interest rate outlook differential and the differences in the performance of each economy, as evidenced by job growth—or lack thereof for Canada as compared to the U.S. We are also very cognizant of the so-called mortgage wall that is coming for Canadian borrowers in 2025 and 2026. Consider this: If mortgage expenses are stripped out of inflation, we are already below 2%. In some respects, the medicine—high rates—has become the poison. Higher interest costs are now causing excess inflation. There is also concern over what the changes in capital gains taxes are going to do to the housing market. In short, being long the CAD at this point is certainly a difficult proposition.

On Gold, we took advantage of the recent rip to sell some upside and purchase some downside protection. We hold a collar on our Gold ETF in some portfolios. If Gold prices get back down to US$2,200, that is an attractive entry point in, what our view is, a multi-year bull cycle—particularly if we see continued inflammation in the rhetoric around deglobalized trade. There are a lot of countries that want to move away from the USD, and they cannot do that unless they hold Gold reserves. So, we have seen a pattern of central bank buying over the past five years, and it appears to be going parabolic.

CAD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

GOLD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Footnotes

1 Duration: A measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as number of years. The price of a bond with a longer duration would be expected to rise (fall) more than the price of a bond with lower duration when interest rates fall (rise).

Disclosures

The viewpoints expressed by the Portfolio Manager represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time without any kind of notice. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

This article is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Investments should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.