Shifting to Neutral: The Case for Optimistic Caution

The winds of change are blowing. In early June, the Bank of Canada (BoC) became the first of the world’s major central banks to lower interest rates, cutting by 25 basis points a day before the European Central Bank (ECB) made the same move.

We believe this is an environment where you don’t necessarily need to be overweight Equities.

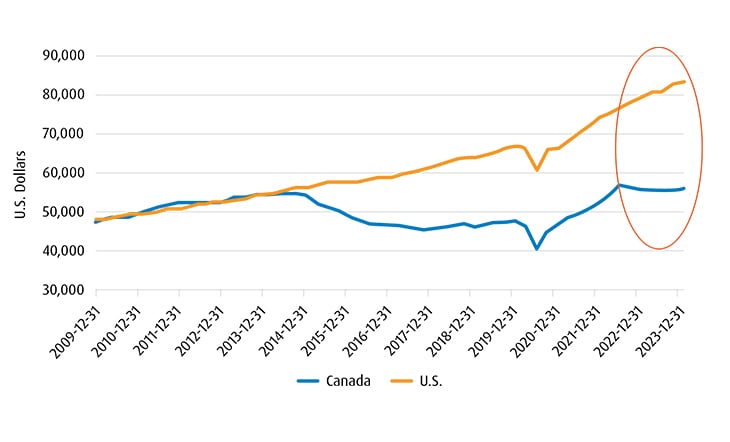

Canada’s Yawning Productivity Gap Taking a Toll

U.S. Outlook

Canada Outlook

GDP Per Capita in U.S. Dollars

International Outlook

EAFE is improving, though still at a modest pace. Emerging Markets (EM), led by China, is still challenged. The trickling of stimulus is helping but there are issues—especially domestically in the latter, with real estate headwinds lingering. China manufacturing is also struggling to ramp up production because it is already producing so much. Chinese manufacturing Chinese manufacturing Purchasing Managers Index readings (PMIs) are struggling to remain above 50—a key gauge that if below that mark, indicates contraction; China is flooding the world with cheap manufacturing goods but it is still in the context of massive excess supply.

Key Risks | BMO GAM house view |

|---|---|

U.S. Recession |

|

Inflation |

|

Interest rates |

|

Consumer |

|

Housing |

|

Geopolitics |

|

Energy |

|

Asset Classes

EQUITIES

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

FIXED INCOME

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

CASH

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Equity

CANADA

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

U.S.A.

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EAFE

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EM

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Fixed Income

In terms of credit spreads on High Yield, they are tight in the U.S. and we expect them to remain so, with growth cooling and not crashing. In Canada, they are less tight and there is scope for improvement as interest rate cuts price in. There is going to be more divergence in bond market pricing between the U.S. and Canada, based in part on the fact that there will likely be more cuts in Canada than what the market is pricing in. A significant driver of why the market isn’t pricing more BoC cuts in, is the perceived limits of that divergence with the Fed. There are definite limits to that divergence, but our view is there is more scope for respective monetary policies to widen over the next couple of years than the market currently appreciates. There is significant mortgage refinancing that is coming in 2025 and 2026. Putting aside timing, the narrative has yet to catch up to the amount of loosening the BoC may undertake.

IG CREDIT

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

HIGH YIELD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

EM DEBT

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

DURATION

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Style & Factor

Factors are bleeding into each other in this market. Value is not necessarily synonymous with Quality and Yield at this point. Microsoft falls into the Growth bucket but it is also one of the best Quality names by virtue of its cash flow generation. Even Nvidia is making money on the cash that it is sitting on right now, and it is very much in growth mode. We’re seeing dividends come out of a number of the key market leaders in the Technology area.

VALUE

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

GROWTH

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

QUALITY

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

YIELD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Implementation

CAD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

GOLD

- Very Bearish

- Bearish

- Slightly Bearish

- Neutral

- Slightly Bullish

- Bullish

- Very Bullish

Footnotes

1 Duration: A measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as number of years. The price of a bond with a longer duration would be expected to rise (fall) more than the price of a bond with lower duration when interest rates fall (rise).

2Volatility: Measures how much the price of a security, derivative, or index fluctuates.

Disclosures

The viewpoints expressed by the Portfolio Manager represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time without any kind of notice. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

This article is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Investments should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.